Authorized donees

- Blog /

- Authorized donees

Published on Monday, August 19, 2024

What is an authorized donee?

They are legal entities formed as civil associations, private charitable institutions or charitable foundations, which have a non-profit purpose and are authorized by the SAT (Mexican Tax Administration Service) to receive income tax-deducible donations.

Among the legal entities mentioned hereabove, trusts with non-profit purposes shall be included as they can be allowed to be authorized donees.

Authorized donees can carry the following activities:

- Assistance

- Education

- Scientific or technological research

- Culture

- Scholarships

- Environmental

- Endangered species breeding program

- Social development

- Economic aid programs

- Public works and services

- Museums and private libraries

For tax purposes authorized donees pay taxes as a non-profit legal entity.

Income that is not considered taxable activities for authorized donees

Income that is not considered taxable activities for Civil Society Organizations (CSOs), and therefore not subject to taxation, includes income received from:

- Donations

- Support or incentives provided by the Federation, state entities, or municipalities

- Sale of fixed or intangible assets

- Membership fees

- Recovery fees

- Interest

- Intellectual property rights

- Temporary use or enjoyment of real estate

- Returns from shares or other securities placed among the general investing public

Income for which you should always pay ISR (Income Tax)

Authorized donees must pay taxes like any other legal entity (Title II of the Income Tax Law), on the following types of income:

- Alienation of assets.

- Receiving interest, regardless of whether it is in foreign currency.

- Winning prizes.

- Providing services to individuals other than their members or partners, if the income exceeds 5% of the total income of the entity for the fiscal year in question.

- Determining or having items assimilated to distributable surplus, also known as fictitious distributable surplus.

The benefits of authorized donees are:

- They are taxed for fiscal purposes as non-profit legal entities.

- They are not income tax contributors as they do not seek to generate a profit.

- They may receive unlimited donations, whether in cash or in kind, from residents within the country or abroad; they must issue the corresponding receipts.

- They may have income not related to their social purpose, provided that such income is less than 50% of the total income for the fiscal year.

Option to obtain income other than donations

When a recipient organization generates income from activities unrelated to the purposes for which it was authorized to receive donations, and this income exceeds 10%, it must calculate the profit generated by these activities and pay tax at a rate of 30%.

Causes for loss/revocation of the authorization to receive donations:

- If recipient organizations generate income from activities unrelated to the purposes for which they were authorized to receive donations, and this income exceeds 50% of their total revenue for the fiscal year, they will lose their authorization. This will be determined by a resolution issued and notified by the tax authority.

If, within 12 months following the loss of authorization to receive deductible donations, the organization does not regain such authorization, they must allocate all their assets to another authorized done to receive deductible donations

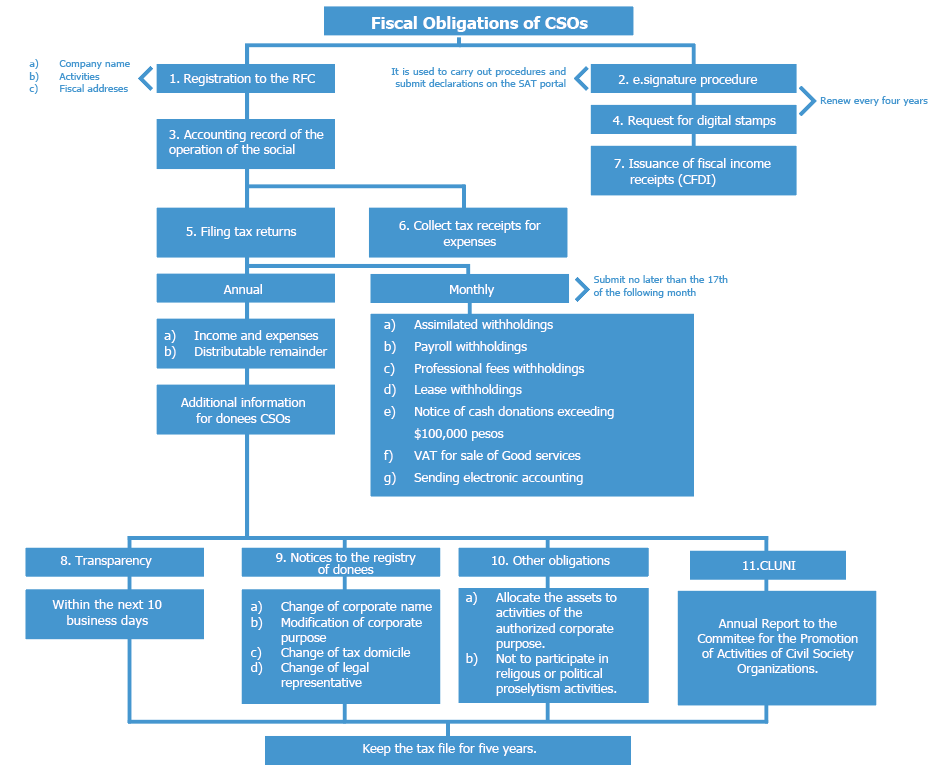

- Failure to submit the required informational returns, which include:

a) The one established in Rule 3.10.10 and Form 19/ISR, “Informational Declaration to Ensure Transparency of Assets, as well as the Use and Destination of Received Donations and Activities Aimed at Influencing Legislation.”

b) The one referred to in Rule 3.10.27 and Form 146/ISR, “Informational Declaration of Donations to Mitigate and Combat the SARS-CoV2 Virus.”

c) The one referred to in Rule 3.13.6 and Form 1/DEC-14, “Support for the Reconstruction or Rehabilitation of Housing in the Areas Affected in the State of Guerrero.”

- Under no circumstances may recipient organizations allocate more than 5% of donations, and, where applicable, any income they receive, to cover their administrative expenses. Administrative expenses are those incurred by NGOs for their internal operations but are not related to the specific activities they undertake. Operational expenses, on the other hand, are related to the organization’s social purpose. (Article 138 of the Income Tax Law Regulations).

- Do not incur in any of the causes for revocation referred to in Article 82-Quáter, Section A of the Income Tax Law.

If you require support with tax compliance, do not hesitate to contact our specialist.

Sincerely,

Kreston BSG® México

For more information, write us at contacto@krestonbsg.com.mx or find the nearest office here.

Our goal is to build a network of trust with our clients to be the support in achieving business objectives. We are a network of firms with a presence in more than 115 countries, experts in offering tax, auditing, legal and accounting consulting services at national and international level. Everything written in this space is for the benefit of the readers; however, for a correct application of specific topics it is necessary to refer to our specialists. For more information visit www.krestonbsg.com.mx