Impairment of assets – Impact of COVID

- Blog /

- Impairment of assets – Impact of COVID

Published on Thursday, October 1, 2020

First publish in International Association of Financial Executives (IAFEI) 49th Issue.

By José García, partner at Kreston BSG México, member of the audit comittee at the firm and Member of the Group Puebla of the Mexican Institute of Finance Executives (IMEF). And Juan Espinosa, partner at Kreston BSG México, member of the quality group of Kreston International LTD an VP of the National Technical Board of the Mexican Institute of Finance Executives (IMEF).

The COVID-19 outbreak has developed rapidly and worse than expected in 2020. Measures taken to contain the spread of the virus, including travel bans, quarantines, social distancing, and closures of non-essential services have triggered significant disruptions to business worldwide, resulting in an economic slowdown. Global stock markets have also experienced great volatility and a significant weakening. Governments and central banks have responded with monetary and fiscal interventions to stabilize economic conditions and it is unknown what the long-term impact on the business may be but for sure it will not be positive for most of the economic participants. If society and, as a consequence, businesses are exposed to COVID-19 for a longer period of time, it may result in prolonged negative results, pressure on the liquidity overall, jeopardizing of going-concern assumption and finally, in impairment of long-live assets as defined by the International Financial Reporting Standards (IFRS), specifically IAS 36 Impairment of Assets. The Latter is addressed in this article.

Impairment basics and indicators

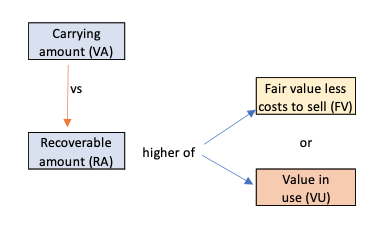

IAS 36 requieres tangible and intangible assets (with certain defined exceptions) to be carried at no more than their recoverable amount. To this end, the entities should test long-live assed for potential impairment when indicators of impairment exist or, at least, annually for goodwill and intangible assets with indefinite useful lives. The recoverable amount (RA) is defined as the higher of fair values less cost to sell (FV) and Value in use (VU). The basic principle of impairment test is to compare the carrying amount (CA) with the RA; if the latter is lower that the CA, an impairment loss should be recognized in the books.

Indicator of Impairment

As mentioned, if impairment indicators are observed, it is likely that the CA of the assets may be impaired. Impairment indicator comprises both external and internal information such as:

- Change in markets interest rates;

- significant adverse changes in the technological, market economic or legal environment in which the entity operates;

- cash flows disruption or observed negative trend;

- material loss of clients and business segments volume;

- loss of purchase acquisition power from the markets in which the entity operates;

- disruption of commercial and production activities, including key suppliers;

- internal restructurings;

- evidence of obsolescence;

- physical damage to the assets;

- governmental adverse measures slowing the participation of economic parties.

As it can be observed, most of the aforementioned impairment indicators are nowadays observed and will prevail in the forthcoming months and/or years, depending the market, region, country and of course, industry; therefore, the question if impairment indicators exist is no longer under discussions and the entities should focus in determining the RA of long-live assets in view of the forthcoming 2020 year-end closing.

Recoverable amount

Fair value less costs to sell - Definition

Fair value less costs to sell (FV) is the amount obtainable from the sale of the assets in an arm's length transaction between knowledgeable and willing parties, less to cots of disposal. The best evidence of FV is a price in a binding sale agreement in an arm's length transaction of the market price of the assets less the costs of disposal. If a market price is not available, FV can be determined using a discounted cash flow approach (DCF), always taking into consideration future events, market conditions, risks related thereto and other pertaining data.

Value in use - Principal premises for its determination

Value in use represent the present value of the future expected cash flows to be generated from an asset or a Cash generated unit (CGU) and comprises two basic elements:

a) Cash flow projections - estimation of the future cash flows that the entity expects from the normal utilization of the long-live assets and expectations on possible variations in the amount or timing of those future cash flows and should consider the following, but not limited to:

i. Based on reasonable and supportable assumptions that represent management's best estimate of the set of economic conditions that will exist over the remaining useful life of the asset;

ii. based on the most recent financial budgets/forecasts approved by management - without including cash inflows or outflows from future restructuring to which the entity is not yet committed to;

iii. not consider borrowing costs, income tax receipts or payments and capital expenditures that improve or enhance the asset's performance;

iv. include overheads directly attributed or that can be allocated on a reasonable and consistent basis to assets;

v. consider the amount of transactions costs if disposal is expected at the end of the asset's useful life; and

vi. for periods beyond covered by the most recent budgets/forecasts, the projections should be based on extrapolations using a steady or declining growth rate unless and increasing rate can be justified.

Some examples of key assumptions used by the companies in determining the cash flows projection are summarized as follows:

Discount rate (time value of money) - represented by

a. A pre-tax discount rate reflecting current market assessments of the time value of money and risks specific to the asset and entity;

b. the price of bearing the uncertainty inherent in the asset which can be reflected in either the cash flow estimation of WACC; and

d. other factors, such as non-liquidity that market participants would reflect in pricing the future cash flows the entity expects to obtain from the related asset.

The determination of an appropriate discount rate reflecting current market assessments, risk of the entity and other external factors, turns out to be very complex and will require undoubtedly judgment and assumptions from top executive and financial management. Furthermore, the professional assistance from valuation experts should not be undervalued.

Impairment loss - recognition

As already mentioned, an impairment loss should be recognized in the financial statements to the extend the CA of the asset exceeds its RA. If assets are kept at historical cost, impairment losses are recognized as an expense immediately in integral result of the year. If the impaired asset is maintained at revalued cost, the impairment loss will decrease the revaluation and recognized directly in other comprehensive income, reducing the related revaluation surplus. If the impairment loss exceeds the revaluation surplus, the remaining loss is charged to the integral result of the year.

If external factors and circumstances indicate or provide significant input on positive changes in the asset's value and market conditions, as compared to those in place when the impairment loss was recognized, the impairment loss previously recognized can be reversed. It his is the case, the adjust CA of the asset cannot exceed the CA of the asset that would have been determined had no impairment loss been previously recognized. Lastly but not least, the asset's remaining useful life, the depreciation method or the residual value need to be reviewed and adjusted if there is an indication that impairment may no longer exist, even if no impairment loss is reversed.

Conclusions

COVID-19 affects on worldwide economy will prevail, at least, in the medium-term, specially in developing countries/economies. As the impairment of assets is one of the core management estimation and judgment processes within the financial reporting, which analysis, determination and assessing are with no doubt complex and time consuming, it is absolutely necessary to establish deadlines for planning, inventory and allocation of resources, wether internal or external as for a proper and timely determination of business planning, forecasting, discount rates and related key element and premises to obtain a reasonable VU.

Likewise, it is important to mention that the top level of entities management should at any time be involved to provide experience, data input, consideration of risks, opinion, different point of views and of course, a consented conclusion if an impairment loss should be accounted for and properly disclosed to the final user of the financial statements.

References:

International Accounting Standards Board (2019. International Accounting Standard 36, Impairment of Assets (IFRS.org).

Related Blogs